Tips from ME: What drives women’s money decisions?

![]()

This article is brought to you by ME.

Research[1] shows women are often motivated by one key driver when it comes to managing money – and it’s not their own financial wellbeing.

Since 2011, industry super fund-owned bank ME has produced a bi-annual study called the Household Financial Comfort Report. Over the years, this study has consistently found that women lag behind men when it comes to financial comfort. And there’s a simple reason why.

According to Roslyn Russell, Research Professor in the School of Economics, Finance and Marketing at RMIT University, women tend to base their financial decisions around the wellbeing of their family, rather than themselves. This can range from their children’s education and caring for elderly parents to providing for grandchildren.

A study Russell co-authored called Women and Money in Australia: Across the Generations found that 80% of women indicated that providing for the daily needs of the family was a high priority.

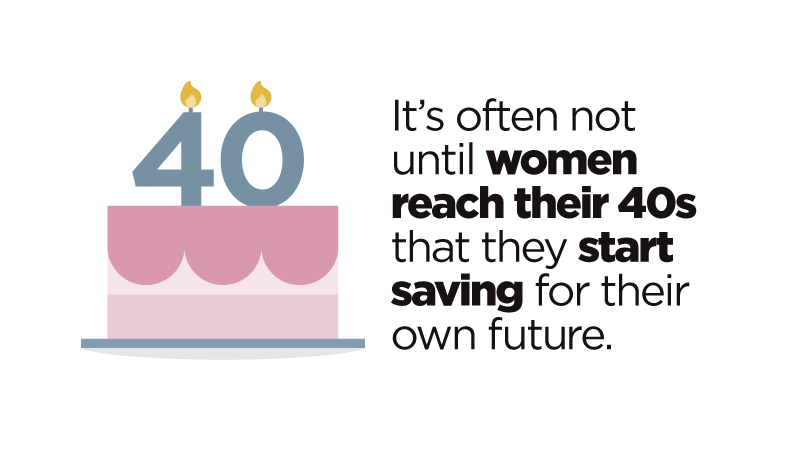

It’s often not until women reach their 40s that they start saving for their own future. By this stage, it can be much harder to achieve financial independence. According to the study, only around 30% of women in their 20s and 30s prioritised their retirement and although this proportion increased to close to 50% in women aged 40–49, retirement still wasn’t being prioritised enough.

Putting the family first

Professor Russell explains: “Women’s finances are strongly connected to emotions, values and beliefs. So it’s not that surprising that the main thing driving the financial decisions of women is caring for the family.”

Along with putting their own financial needs last, many women even feel a sense of guilt when they spend money on themselves.

This pattern of behavior can impact a woman’s personal savings, potentially leaving her financially vulnerable as she ages.

Personal wellbeing matters too

The thing is: making space for personal financial needs is not being selfish.

On the contrary, when a woman improves her own financial wellbeing, she can be less likely to rely on anyone else for financial support later in life.

Don’t overlook your own money needs

Taking care of your own financial health doesn’t have to be synonymous with neglecting the wellbeing of your family. Taking the three simple steps below can be the key to a financially fitter you.

- Aim to grow savings

Sure, it can be difficult to find savings when there’s not much cash to spare. But setting just a few dollars aside into a savings account each pay day can be the start of something big – a savings pool for the future.

Growing savings is not just good for your financial health. Professor Russell says: “Saving is like magic. There’s a psychological benefit to saving, and it provides you with a sense of security.”

- Set some goals

Mapping out financial goals is important. This gives you something to work towards, and benchmarks to tick off as they are achieved. Make your goals clear and specific, and share them with a friend or family member – it can help you stay accountable and motivated.

“Mapping out your financial goals, including where you want to be in the future when you retire, can contribute to a happier and more secure financial life later on,” Professor Russell says.

- Get to know about money matters

If you’re not sure where to start with improving your money management skills, take advantage of the wealth of resources available, including Ed – ME’s free online school of money. The more you know, the better placed you are to make informed decisions about how to spend and save your money.

Spread the word

Be sure to share your money learnings with the other women in your life. In particular, when women teach their daughters the value of financial independence, the result can be a powerful exchange of knowledge that helps to close the financial comfort gap.

This article is brought to you by ME. For more information, please visit www.mebank.com.au

Members Equity Bank Limited ABN 56 070 887 679 AFSL and Australian Credit Licence 229500.

[1] http://researchbank.rmit.edu.au/view/rmit:40136