Tips from ME: Five first home buyer traps to avoid

![]()

This article is brought to you by ME.

The number of first home buyers in Australia’s housing market has hit a six-year high, according to new ABS data[1], but when it comes to buying a home, errors can prove costly.

Industry super fund-owned bank ME highlights five key pitfalls that first home buyers need to be aware of.

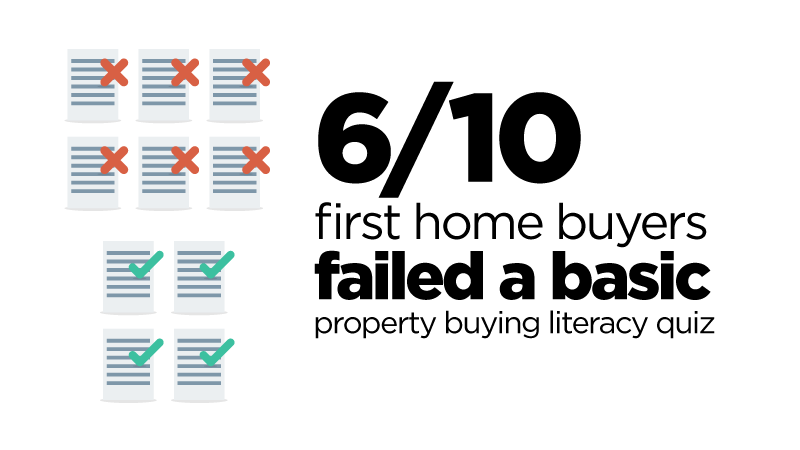

- Buying blind

Buying a first home is a big deal, so it makes sense to be clued up on what’s involved.

Yet, research by ME found six out of ten first home buyers failed a basic property buying literacy quiz.

Key knowledge gaps included understanding that lenders’ mortgage insurance protects lenders – not

borrowers – and that there’s no cooling off period when buying at auction.

When it comes to the biggest purchase of your life to date, it pays to know the basics and get a handle on the terminology. Head to the government’s MoneySmart website[2] and ME’s free online school of money, Ed, to get up to speed – fast.

- “Guesstimating” your borrowing power

Don’t go home hunting based on a hunch about how much you can borrow. It could see you waste a whole lot of time and money checking out homes you simply can’t afford.

The only way to know for sure how much you can borrow is to speak with a lender or mortgage broker.

- Not sticking to your budget

It can be easy to buy with your heart rather than your head, but this brings the risk of blowing your budget.

A property survey by ME found one in five (22%) home buyers exceeded their buying budget. Of these, 46% overstepped their budget by $30,000 and 30% blew their budget to the tune of $50,000. Ouch!

An easy way to stay focused on what, and where, you can afford to buy is by having your home loan conditionally approved – it draws a very clear line in the sand.

Conditional approval also means your loan is pretty much ready to go when you find the place that’s right for you, and that can mean enjoying a headstart over less organised buyers.

- Overlooking upfront costs

Buying a home comes with a range of upfront costs including legal fees, pre-purchase inspections and stamp duty.

Sure, first home buyer grants and concessions can help to cover at least some of these add-ons. But it’s a smart move to factor upfront costs into your buying budget so you can avoid nasty surprises that could see you scrounging for cash later on.

- Assuming all loans and lenders are the same

Home loans are not a one-size-fits-all product. Different lenders not only charge different interest rates, they also offer a variety of home loan features.

These features matter because they can make your home loan easier to live with, and help you become mortgage-free sooner.

The bottom line is, when it comes to a home loan, it can pay to look beyond the lender you’ve always banked with.

If you can avoid these five mistakes, you’re well on your way to enjoying a stress-free home buying experience.

This article is brought to you by ME. For more information, please visit www.mebank.com.au

Members Equity Bank Limited ABN 56 070 887 679 AFSL and Australian Credit Licence 229500.

[1] https://www.news.com.au/finance/real-estate/brisbane-qld/first-home-buyers-hit-6-year-high/news-story/3f316f7473c933f8392859ea22c0013d

[2] https://www.moneysmart.gov.au/